The RWA Vision Explained with Data: Why Finance is Better Onchain

RWAs are making traditional finance better onchain, from onchain institutional lending to stablecoin yields. See the data for yourself.

At ETHDenver 2025, we teamed up with our partners at Plume for their RWAfi Summit. Plume is building the world’s biggest rollup for RWAs, or real world assets – the term covering the many TradFi products we want to bring onchain. Equities, bonds, treasuries, real estate, commodities – any asset class you can think of can and will trade onchain.

But why is finance better onchain? That’s the question we set out to answer on our panel at RWAFi, alongside experts from Maple, OpenTrade, and Qiro, moderated by Wintermute BD and Partnerships Director Katryna Hanush.

Why is onchain finance the future?

— Plume - RWAfi L1 ✈️ DAS 2025 (@plumenetwork) February 25, 2025

Our next panel is about to tackle the shift from TradFi to DeFi and what makes onchain finance more efficient, transparent, and scalable.

Featuring:

🎙️ Luke Chmiel @talkintokens | Associate Director, @maplefinance

🎙️ Jeff Handler @BTC_Jeff |… pic.twitter.com/VCquRZEGq6

The insights panelists shared are illuminating to anyone who wants to learn about RWAs and what they mean for the future of finance. We’ll break some of them down here, along with some supporting onchain data.

Democratization of institutional investment products

Panelists cited greater accessibility as one of the key benefits of putting TradFi onchain with RWAs. By cutting out the middlemen of the traditional finance world and doing away with exclusionary practices like investment minimums, DeFi can give the average investor access to financial products that have traditionally only been available to institutional players.

Institutional private credit is a great example. Loans to businesses are attractive investments because they offer stable returns with relatively low volatility, but often get higher yields than public fixed-income products. But because of the administrative complexity and intermediaries involved, institutional private credit has mostly been restricted to large investment funds and high-net worth individuals, keeping retail sidelined.

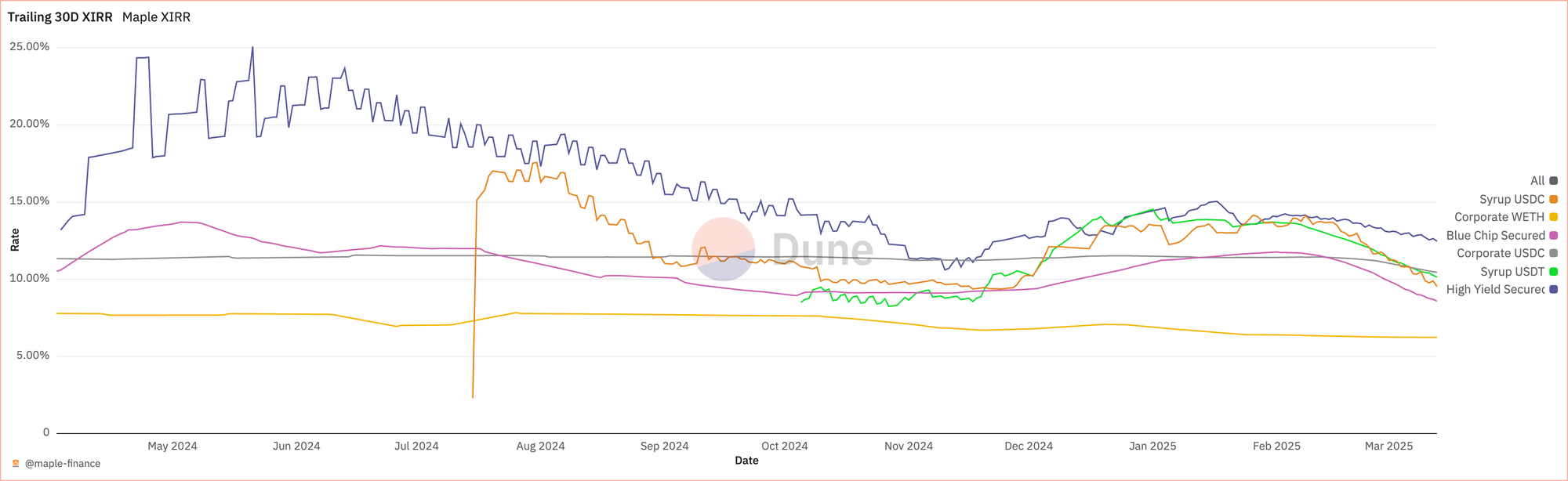

On the panel, Maple Finance Associate Director Luke Chmiel discussed how his company is changing this. Chmiel said that putting institutional private credit onchain makes smaller deal sizes economical, opening up access to investors of all sizes, with recent returns between 10% and 25%.

Onchain data shows this democratization in action. Since 2023, investors of all sizes have deposited to Maple’s onchain institutional lending pools.

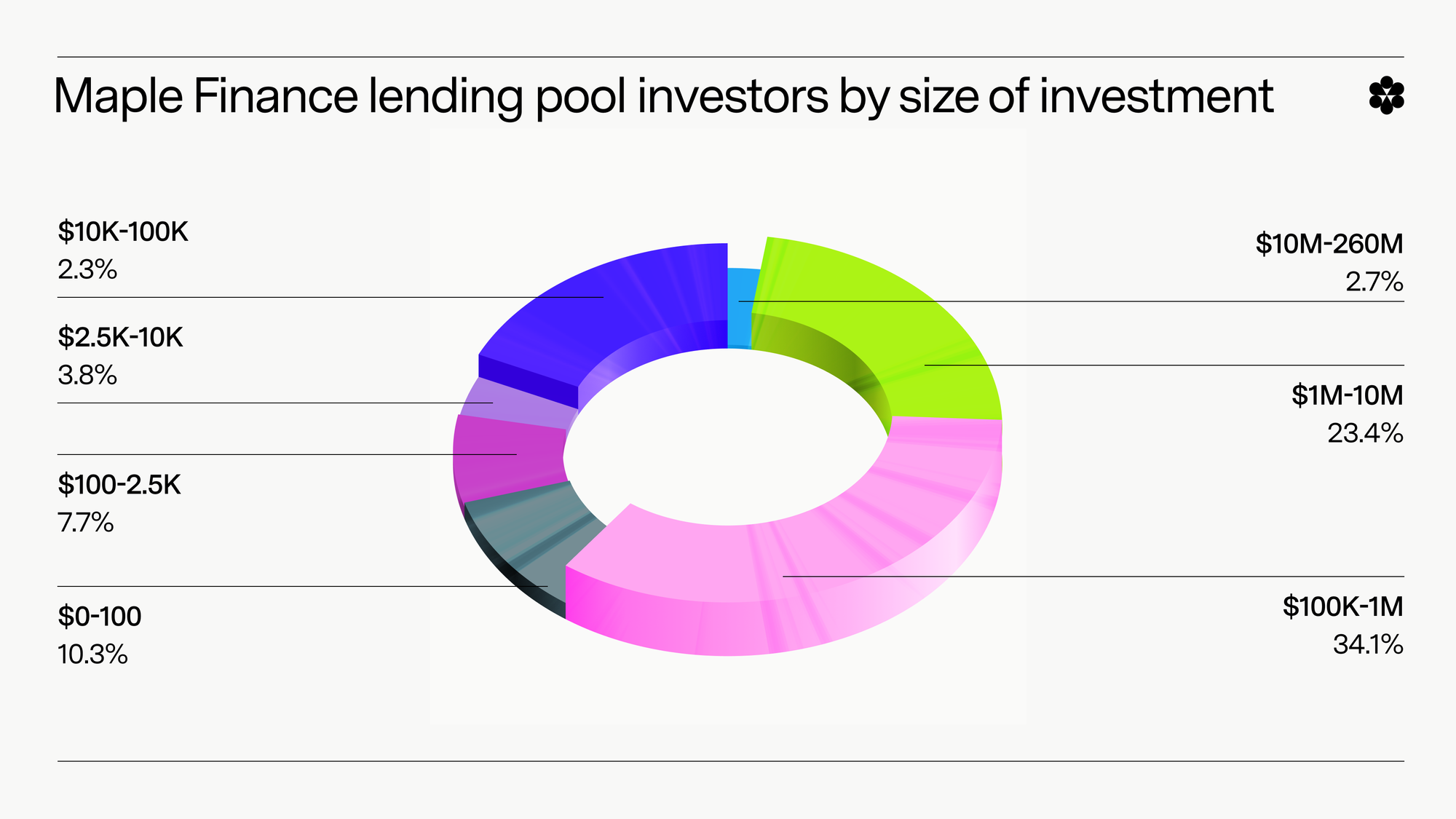

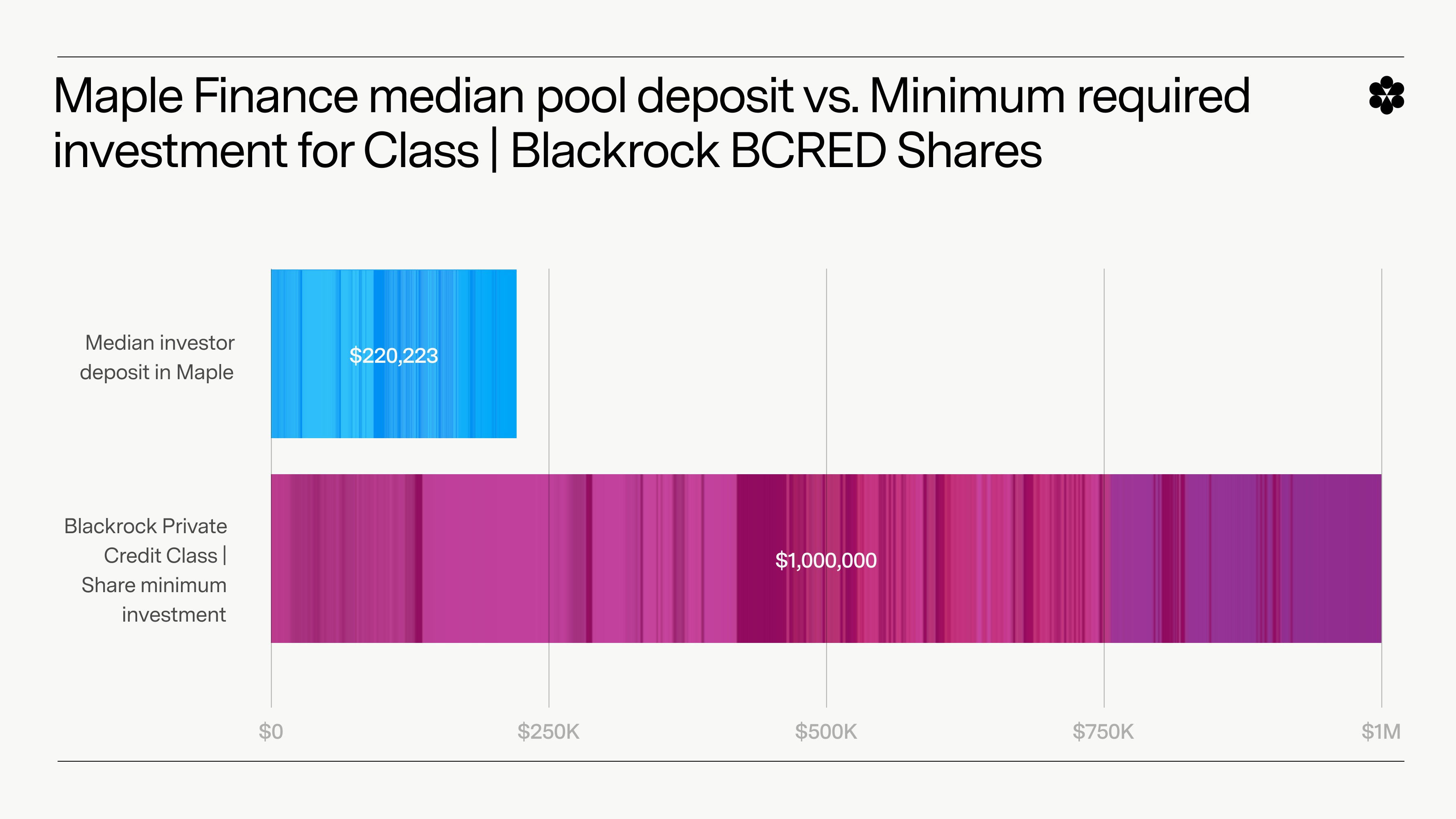

For comparison, let’s look at the Blackstone Private Credit Fund (BCRED), a major institutional credit product in TradFi. According to its prospectus, Class I shares in BCRED require a $1 million minimum investment. Even the lower-level Class S and D shares have their own minimum of $2,500. 74% of Maple lenders are investing below the $1M BCRED minimum, getting access to a comparable institutional private credit product at a much lower financial commitment. 18% are even investing below the $2,500 minimum for Class S and D BCRED shares. But Maple isn’t just targeting retail – nearly a quarter of its lending pool depositors are investing at institutional size, with the biggest putting up over $250 million.

Where else besides onchain RWAs do you see retail investors and deep-pocketed institutional lenders using the same sophisticated financial products?

Overall, Maple’s median investment of $220,000 is much lower than the mere minimum for Class I BCRED shares. We don’t have the data necessary to calculate BCRED’s actual median Class I investment size, but it’s certainly much higher than the $1M minimum.

We’re still in the early innings of RWAfi, but the Maple vs. Blackstone comparison shows that DeFi is already making some of TradFi’s most attractive institutional investment products available to the little guy.

Stablecoin yields give underserved populations new opportunities

While RWAs are considered an emerging crypto use case by many, there’s one type of RWA that’s already crypto’s biggest use case: Stablecoins. Stablecoins pegged to the U.S. dollar are perhaps the most widely adopted crypto product today, especially among non-crypto native users in countries with less financial stability. Countries facing currency devaluation in regions like Latin America and Africa have seen widespread stablecoin adoption as a means of protecting savings.

During the panel discussion, OpenTrade CCO Jeff Handler pointed to an emerging use case that builds on this success: Stablecoin yields in conventional bank accounts. OpenTrade is already piloting this concept in Colombia through a partnership with neobank Littio. Users who sign up for the product deposit fiat currency like they would with any other bank account. But under the hood, the money is converted into USDC and deposited into one of OpenTrade’s stablecoin yield vaults, which accrue interest from OpenTrade’s holdings in U.S. Treasury Bills, and USD Money Market Funds. The user doesn’t have to interact with the blockchain directly. There are no seed phrases or wallets to keep track of – they just see the interest add up in their bank account.

According to RWA.xyz, OpenTrade’s Flexible Term USDC Vault is providing 4% APY interest on USDC deposits. Let’s use that number plus data on the Colombian Peso-U.S. dollar exchange rate to compare results for a Littio user taking advantage of OpenTrade’s stablecoin yield vaults versus someone who deposited Colombian Pesos (COP) in a standard bank account.

A user depositing $1,000 USD worth of COP in the Littio account with OpenTrade would see stable growth to $1,040 one year later. $1,000 of COP sitting in a standard account, however, would be worth just $950 after one year, with lows of $867 in November.

The data illustrates how valuable yield-bearing stablecoin products can be to residents of economically unstable countries, and why they may be RWAfi’s first killer use case.

Permissioned DeFi let institutions get onchain with compliance and security protections

While benefits like those outlined above are enticing to TradFi, there’s a perceived risk around issuing institutional financial products on permissionless blockchains. But as our panelists discussed, the composability of DeFi gives institutions ways of enforcing security and compliance precautions onchain, while still benefiting from the decentralization of Ethereum and other permissionless L1s. This can be done at the app, asset, or blockchain layer in the case of L1s or L2s:

- App layer. Institutions can build permissioned apps on permissionless blockchains like Ethereum, which require KYC/AML checks to use.

- Asset layer. New token standards like Ethereum’s ERC-3643 allow users to launch RWA tokens with built-in rules for who can hold and trade them, including a decentralized identity framework.

- Blockchain layer. Institutions building their own chain from scratch can make several modifications to enforce compliance permissions, such as permissioned validator sets and KYC rules. Rollups building on Ethereum can even utilize a custom gas token outfitted with its own permissions to effectively control who can bridge to the rollup without actually tweaking the chain itself.

Several projects targeting institutions are already implementing these features and gaining traction. Plume Network, for example, has more than $96M in pre-deposits for its upcoming RWAfi rollup, which will act as the hub for projects tokenizing equities, bonds, commodities, real estate – any RWA you can think of.

Source: @plumenetwork on Twitter

While Plume’s blockchain will be open and decentralized, the team is implementing features like ERC-3643 to give institutions flexibility in permissions around RWAs they issue on the chain.

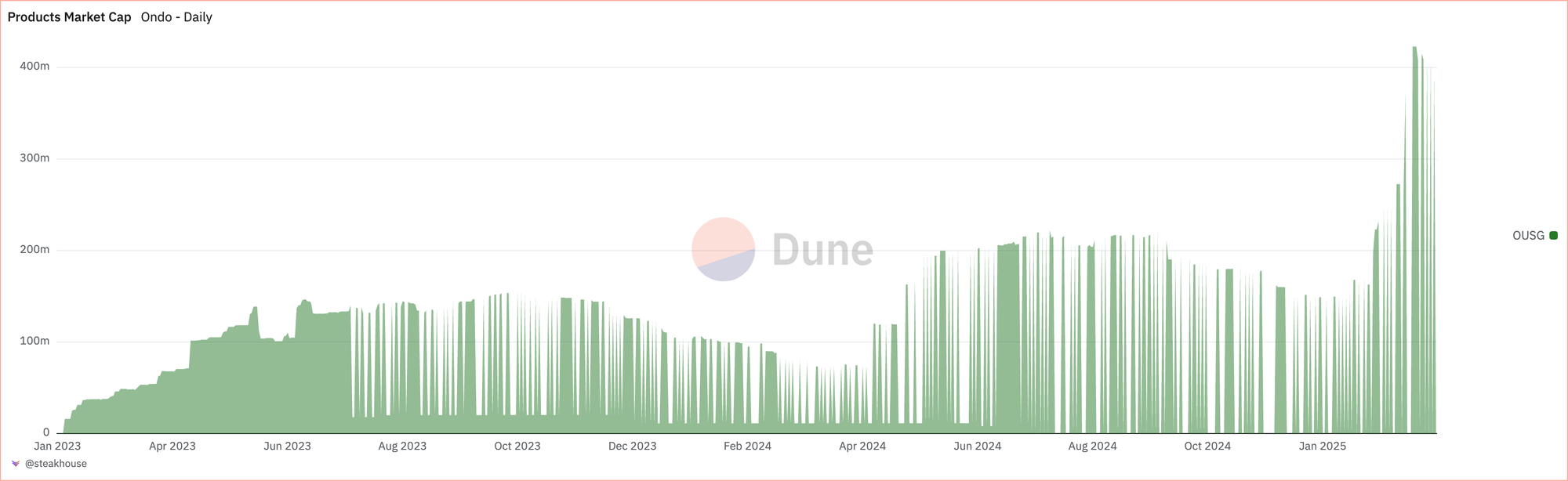

Ondo Finance is another example. While Ondo’s focus so far has been tokenizing U.S. government bonds, the plan is to enable tokenization of other RWAs as well. So far, growth has been strong.

Source: @steakhouse on Dune

Like Plume, Ondo has also built in permissions tooling to support institutions, starting with the token distribution layer of its Global Markets protocol. More recently, however, Ondo announced plans to launch its own Ondo Chain to provide even better institutional protections, as well as to implement more institution-friendly DeFi tooling and avoid the fee volatility of public blockchains.

RWAs are already making finance better onchain

The panel discussion at RWAfi, as well as the supporting data we’ve shared here, tell a clear story: RWAs are already making TradFi better onchain. Even today, at a time when RWAs are a relatively new concept, existing onchain products are democratizing access to institutional investment products and opening up more asset classes to more people, while still giving traditional financial institutions the compliance and security assurances they need to operate.